Health Insurance Options (Part 3):

In the third part of the insurance series, we are discussing health insurance options.

First, you must determine what you are eligible for when it comes to health insurance.

Are you eligible for Medicare?

If yes, insurance offered through Medicare is an option. You should take into consideration whether you or your spouse are eligible through a group health insurance plan before enrolling in Medicare.

If no, you should explore options given to you by your employer (group or retiree health insurance). Shopping the Health Insurance Marketplace can also offer you coverage until you are eligible for Medicare. We do not provide recommendations when it comes to which type of plan to get, but we have a referral who can assist you if you are interested in learning more.

It is also important to know that you may enroll in COBRA for specific reasons (i.e., retiring if group plan had more than 20 employees), which is a continuation of your group health insurance policy up to a certain amount of months, but you will incur the full cost (your portion and the employer’s portion), plus a small fee.

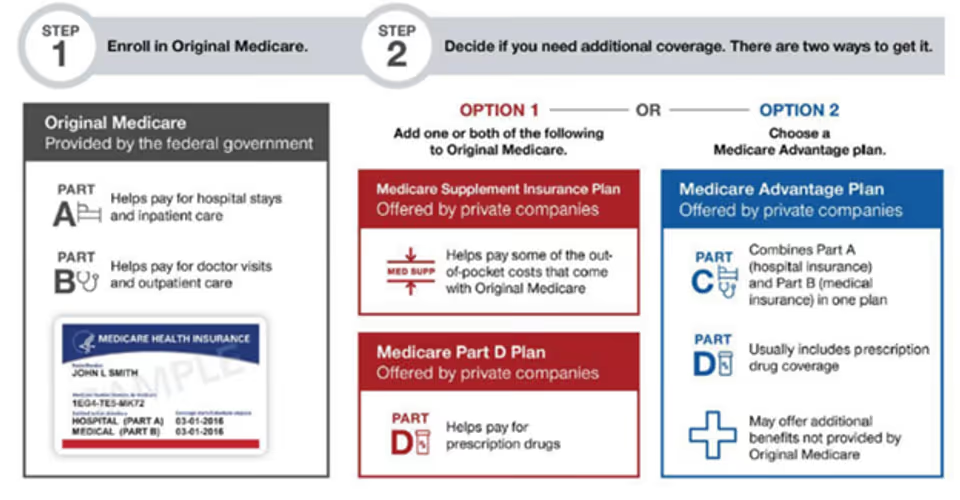

Below is more information regarding Medicare and the key things to know before you shop for supplemental or Advantage plans.

Medicare Planning

Healthcare planning is a key part of the overall retirement planning process. There are several ways that retired individuals can pay for health care. For the majority of Americans aged 65 and older, most health care is provided through the various elements of the federal government’s Medicare programs.

What Does Original Medicare Cover?

- Part A: Covers 80% of Medicare-approved charges after the Part A Deductible ($1,556 in 2022) for inpatient hospital, skilled nursing care, hospice, and related services and equipment.

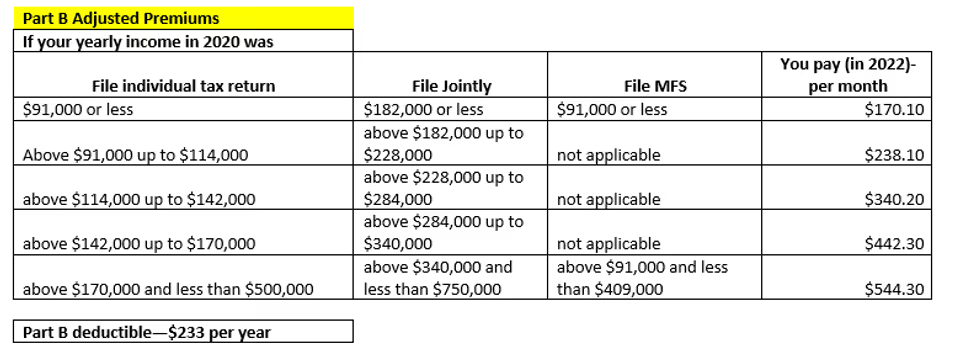

- Part B: Covers 80% of Medicare-approved charges after the Part B Deductible ($233 in 2022) for doctor and outpatient services including labs, diagnostic tests, durable medical equipment, and medications given in a doctor’s office.

- There is no limit or cap on the 20% cost share paid by the consumer.

- There is no coverage for prescription drugs (self-administered).

- There is no or very limited coverage for routine dental, vision, or hearing care.

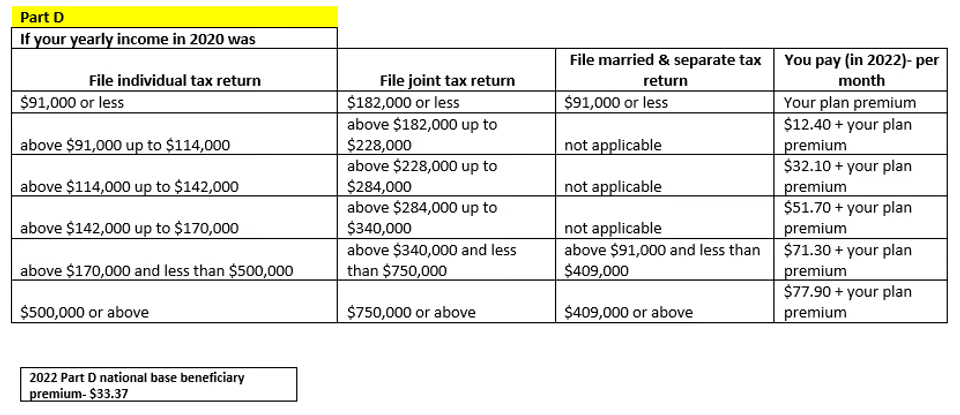

- At the bottom of the page, you will find a chart that provides estimated costs for Part B & D, based on your income level.

Beyond Original Medicare

Part D

- Medicare Part D is a government/private program covering prescription drugs. The plans are offered by private companies through contracts with the federal government.

- If you don’t buy when you are first eligible and want to buy it later, there generally is a lifetime penalty to pay.

Part C (Medicare Advantage)

- Also known as Medicare Advantage plans. These are offered through private insurers through contracts with the federal government.

- These plans include Part A and Part B and usually provide other coverage, including prescription drugs.

- Medicare Advantage typically costs less upfront and potentially more overall if you need lots of medical care.

- These plans are typically network based, potentially restricting provider or facility access; some may require referrals to specialists or have other “gatekeeper” features generally found in managed care plans.

- If you switch from Medicare Advantage to traditional Medicare, you often don’t have guaranteed access to Medigap policy. That means the insurer may charge you more, exclude preexisting conditions for a time or not issue you a policy at all.

Medicare Supplement (Medigap)

- Medicare Supplement plans are a common way to fill in many of the Original Medicare coverage gaps; these plans cover some or all of what Medicare doesn’t pay.

- Plan G is the most comprehensive, popular, and expensive plan available to individuals becoming Medicare-eligible on or after 01/20.

- Plans are standardized across all companies; a Plan G from one company is identical in coverage to a Plan G from another. Difference is initial cost, renewal rates, and customer service.

- Medigap plan owners can choose any doctor or hospital that accepts Original Medicare.

- Maximum flexibility, minimum potential friction.

- No drug coverage.

That means there are two routes to fill the Original Medicare gaps.

1. Medicare supplemental +Part D

2. Medicare Advantage