Intro:

Oftentimes, people do not know what is included in their paystub which can lead to missing errors and not fully understanding what benefits and deductions you have with your employer. This post serves as a guide for understanding your paystub and some of the common line items found within it.

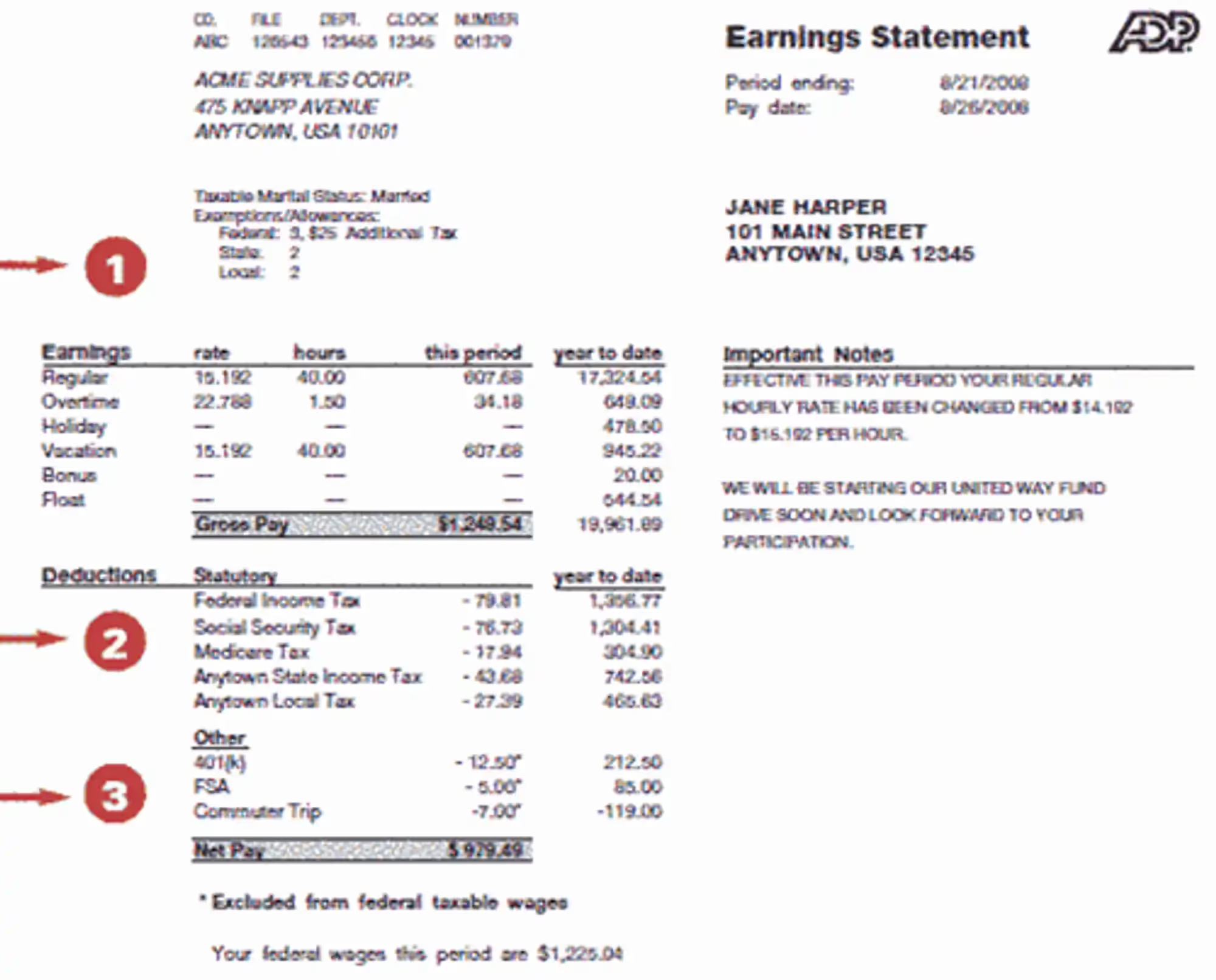

1. Personal Information & Earnings

- Make sure the pay stub is yours. Check the listed address.

- Your pay frequency is also listed here. The begin and end dates should indicate the pay period (weekly, bi-weekly, semi-monthly, or monthly). Knowing this information can help you determine pay periods and calculate estimated annual totals.

- Exemptions/Allowances: This section shows your intended tax filing status, number of tax allowances/exemptions, and additional withholding amounts. You can request changes to your withholding by submitting a Form W-4 to your employer. The IRS offers an online calculator to help you determine your withholding election. In addition, you should review your state and local tax withholding if applicable.

Earnings

- This part reflects all your hard work! This section includes your pay period amount and the amount you’ve earned since the beginning of the year (YTD).

- You may receive a consistent base salary and additional compensation for any of the following sources:

- Performance Bonus

- Retention Bonus

- Stock Compensation

- Commissions

- Severance Pay

- Taxable Fringe Benefits

- Transportation/Mileage

- Cell Phone

- Fitness Center

2. Deductions

- Federal Income Tax: Gross earnings not deducted pre-tax are included in your taxable income. Wages subject to federal income tax are reported in Box 1 of your Form W-2, and withheld taxes are shown in Box 2. The amount listed on this line represents what is withheld for federal income tax. This is deducted each pay period, so you do not have a large tax bill when you file your tax return. When you change your withholding/allowances on your W-4, this tax amount will adjust.

- Social Security Tax: Your gross earnings up to the annual wage base ($147,000) in 2022 are subject to 12.4% Social Security tax. You pay 6.2% as the employee, and your employer pays the other half. Your Social Security wages and taxes will be shown on your Form W-4 in boxes 3 and 4.

- Medicare Tax: Your gross earnings are subject to 2.9% Medicare tax. This tax is also split (1.45% each), like the Social Security tax. If your gross earnings exceed $250,000 (married) or $200,000 (single), a 0.9% Additional Medicare Tax is imposed on earnings above the threshold.

- State Tax: This is the amount your employer withholds to pay your state income tax (not all states have this). This is deducted each pay period so you do not have to pay a large amount when you file your tax return.

- Local Tax: This is similar to the state and federal tax withheld. A local tax is an assessment by a state, county, or municipality to fund public services.

3. Other Deductions (some deductions not listed in image above)

- Once your gross pay is calculated, employee-benefits are deducted. Some of these deductions are pre-tax (denoted with a “ * ”), which means they are excluded from your taxable income on form W-2 and cannot be deducted again on your tax return. Post-tax deduction reduces your net pay but are still subject to taxation

- Retirement Plans: You may contribute to mandatory or voluntary defined contribution retirement plans, such as pre-tax (traditional) 401(a), 401(k), 403(b), or 457(b). These contributions are excluded from taxable income, meaning they reduce your taxable income. Your employee contributions are not subject to income tax, but they are still subject to payroll tax (SS and Medicare tax). Future distributions from traditional retirement accounts will be included in taxable income, subject to ordinary income tax rates. Roth and other after-tax contributions are subject to income tax in the current year but may be distributed tax-free in retirement.

- Medical/Dental/Vision Insurance: Your employer may offer pre-tax benefits, known as Section 125 Cafeteria Plan. These premiums are excluded from income and payroll tax. The total cost of employer-sponsored health coverage is shown on your Form W-2, Box 12, with Code DD. Before terminating employment, multiply this amount by 102% to estimate your potential annual COBRA cost.

- Health Savings Account: If you are enrolled in a HSA-eligible health plan (HDHP), you and your employer can make pre-tax contributions to your HSA. Contributions made through payroll are excluded from income taxes and payroll taxes.Reminder: There are annual contribution limits for individual and family HSAs. You cannot further deduct these contributions on your tax return.

- Flexible Spending Account: You may contribute to pre-tax health care, limited use, or dependent care FSAs, also excluded from payroll taxes. These also have contribution limits, and unlike HSAs, cannot be indefinitely carried over to future years.

- Group Term Life (GTL) Insurance: This means your employer has elected to pay your beneficiaries a portion or a full amount of your annual salary. The employer-paid cost of benefit coverage in excess of $50,000 is included in your taxable income even though you don’t receive the funds. This taxable part is considered imputed income and is reported on Form W-2 as taxable wages.

- Disability Insurance: Most policies are limited to 60% of earnings up to a monthly maximum. The way these benefits are taxed can vary. If the employer reports the premium cost on the worker’s W-2 as imputed income, the worker will pay taxes on that amount, but the benefits would be received tax-free. If the employer does not report the premiums as imputed income, the worker will have to pay taxes on any payouts received.

4. Net Pay

- After employee deductions and taxes are withheld from your gross earnings, the remaining amount is your net pay and will be presented to you by physical check or direct deposit. Setting up automatic savings by directing a portion of your net pay to a savings or investment account is a great way to stay financially disciplined.

Sources:

https://measuretwicemoney.com/how-to-review-a-pay-statement/