Reasons for Making a Charitable Gift:

- Compassion for those in need

- Religious commitment

- Continuation of one’s beliefs, values, and ideals

- Support for the arts, sciences, and education

- A longing to share one’s good fortune with others

There are numerous ways to give to charities. Below are Narwhal’s most popular strategies when it comes to charitable giving.

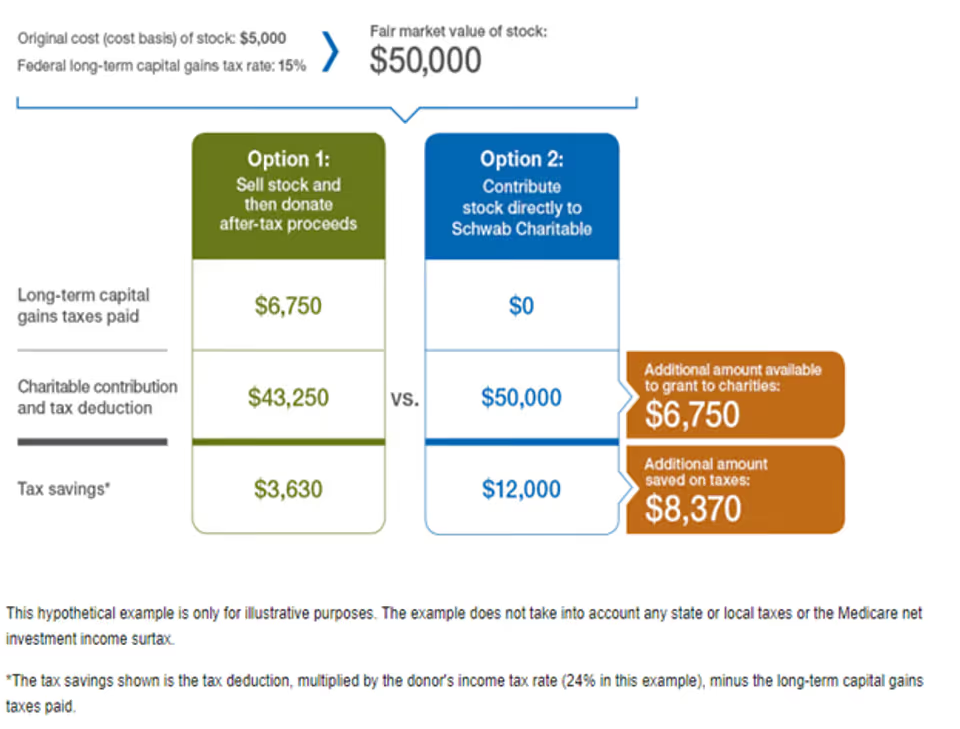

1. Give appreciated non-cash assets instead of cash

This strategy is advantageous for those who itemize their tax deductions. In addition to claiming a deduction for the fair market value of an asset, donors can potentially eliminate the capital gains tax they would otherwise incur if they sold the asset and donated the cash proceeds. This results even more going to the charity and less to taxes. See example in figure 1 below.

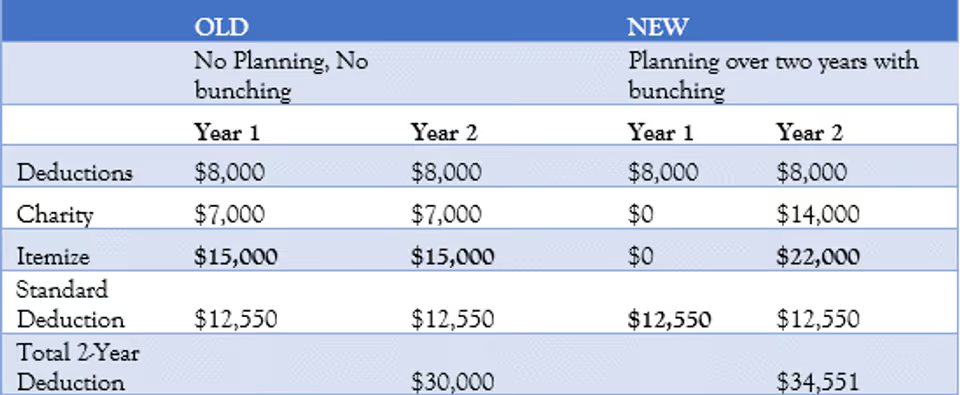

2. Bunch itemized deductions

Some donors may find that the total of their itemized deductions for a certain tax year will be slightly below the level of the standard deduction. You may find it beneficial to bunch two tax years of charitable deductions into one year and take the standard deduction on the other year. See example of bunching in figure 2 below.

3. Make a Qualified Charitable Distribution of IRA assets

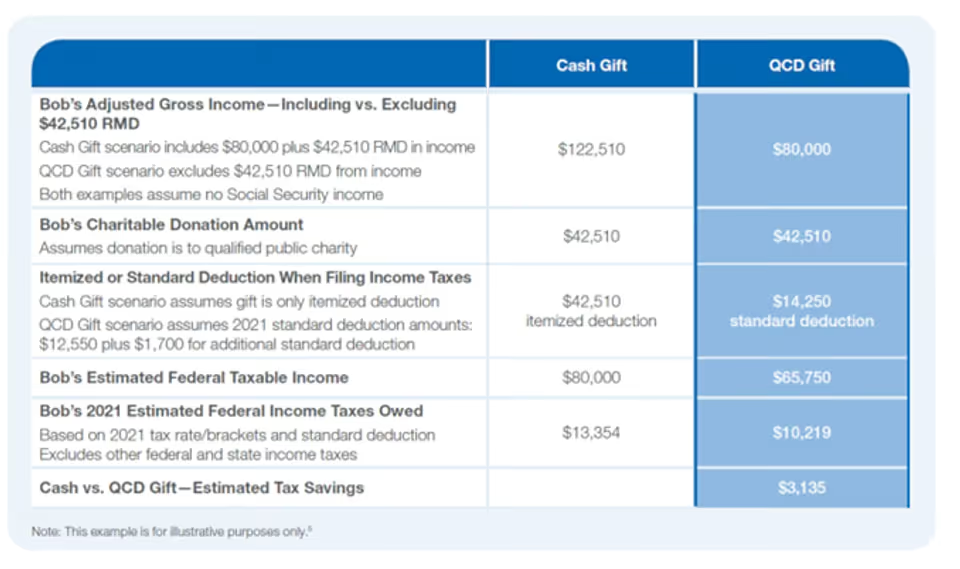

Whether you itemize or claim the standard deduction, if you are age 70 ½ or older, you can direct up to $100,000 per year tax-free from your Individual Retirement Accounts (IRAs) to operating charities through QCDs. By reducing the IRA balance, a QCD may also reduce the donor’s taxable income in future years, lower the donor’s taxable estate, and limit IRA beneficiaries’ tax liability. See below for an example of a QCD and the tax implications of such.

As an example of the potential tax savings of a QCD, consider a hypothetical donor, Bob, who is a single tax-filer with anticipated ordinary income of $80,000 in 2021. Bob is 73 years old in 2021 (which means he falls under the old RMD rules) and takes a distribution from his traditional IRA. In this instance, Bob's IRA is valued at $1,050,000, resulting in a projected RMD of $42,510 ($1,050,000 divided by the IRS mandated age 73 distribution period amount of 24.7). The figure 3 below for an illustration comparing a cash gift of $42,510 with a QCD for $42,510.

Sources:

https://www.schwabcharitable.org/non-cash-contribution-options/making-qcds

https://www.schwabcharitable.org/maximize-your-impact/2021-strategies

Index:

FIGURE 1: Donating vs Selling Appreciated Stock Positions

FIGURE 2: Tax Benefit of Bunch Itemized Deductions

FIGURE 3: Qualified Charitable Distributions of IRA Assets